Amazon’s New Org Chart Is Measured in Megawatts

Yesterday’s story did not read like a typical layoff announcement. It read like a capital plan. Amazon tied roughly 14,000 corporate job cuts—about 4% of its white‑collar ranks—to an accelerated pivot into generative AI, and suddenly the company’s headcount looked less like a staffing table and more like a budget line item under “compute.” The message was unambiguous: fewer people in the back office, more chips, more data centers, more power.

The timing tells its own tale. After weeks of internal emails and a Reuters scoop laying out a restructuring that could extend into 2026, the narrative resurfaced into the weekend with a sharper edge: this isn’t belt‑tightening for a slow quarter, it’s a resource conversion. CEO Andy Jassy has been previewing it all year—generative AI will shrink certain corporate functions—and now the numbers are walking it through the door. Amazon says it has more than a thousand gen‑AI services in motion. The checkbook reflects it: multi‑billion‑dollar commitments to cloud and AI infrastructure, including a $10 billion campus in North Carolina and parallel projects in Mississippi, Indiana, and Ohio.

The calculus behind 14,000

Inside the company, most of the affected employees get 90 days to land another role before severance and transition support begin. It’s a familiar ritual across tech, but this time the denominator is different. Amazon’s corporate base sits around 350,000 within a total workforce of about 1.56 million, yet the new openings are not primarily on adjacent teams—they’re in cold aisles and construction zones. The enterprise that once scaled by adding program managers is now scaling by adding megawatts.

Analyst Neil Saunders described it as “a tipping point away from human capital to technological infrastructure.” It’s a clean phrase for a messy maneuver. In the short run, the company is trimming in devices, advertising, Prime Video, HR, and even AWS’s own corporate layers—precisely the domains where generative AI can collapse workflows, automate routine approvals, and stitch together reporting that once chewed through headcount. In the same quarter, AWS grew 17.5%. The revenue engine is loud enough to drown out the worry—if you’re a shareholder. If you’re inside an affected org, the 90‑day window doubles as a countdown to an org design where your old job now looks like a prompt.

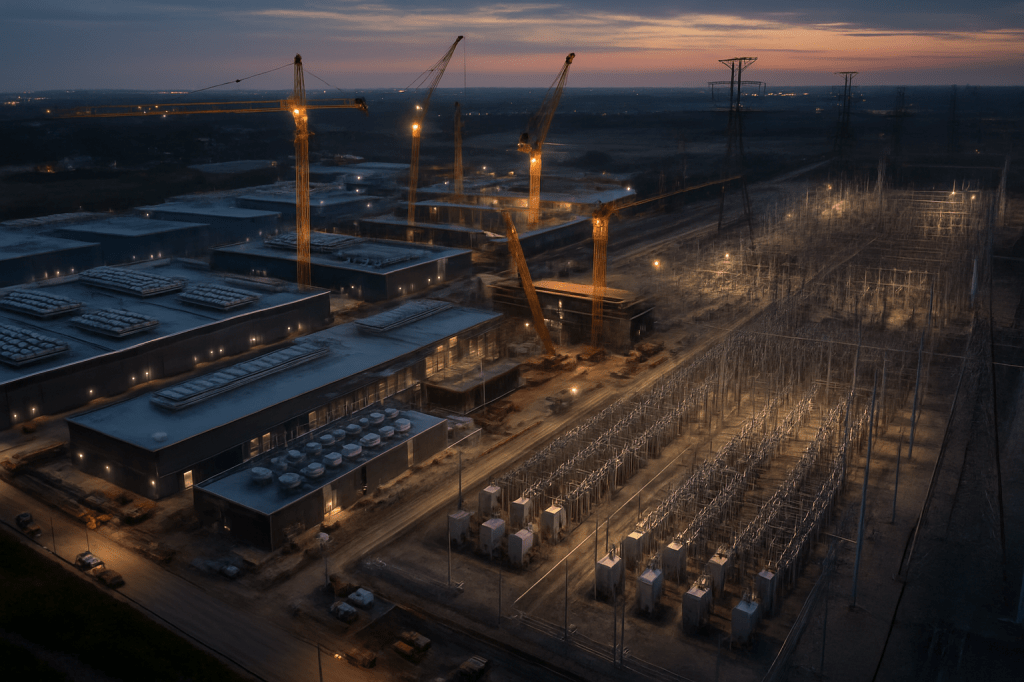

Where the jobs go when the office lights dim

Follow the money and you end up far from HQ. Data center build‑outs pull employment into construction, electrical work, fiber, cooling, and round‑the‑clock cloud operations. States are courting these projects with land, tax incentives, and infrastructure assurances because the secondary economy—contractors, utilities, local services—arrives with them. The employment mix tilts from spreadsheets to substations. That is not a euphemism. When a firm the size of Amazon chooses to automate large swaths of corporate process while pouring cash into power‑hungry facilities, it creates an immediate labor migration from white‑collar hubs to energy corridors.

This is the part of AI disruption that often gets misread. We talk about “AI jobs” and picture prompt engineers in hoodies. The payroll says otherwise. AI’s growth path hires as many electricians and heavy‑equipment operators as it does ML ops engineers. In Amazon’s case, the near‑term backfill for displaced corporate roles isn’t in the headquarters tower; it’s on a construction timetable synced to substation upgrades. That’s why, even while cutting corporate roles, the company can plan to hire a quarter‑million seasonal workers and still claim a net gain in economic activity. The categories have shifted.

The new back office has no chairs

Strip away the press cycle and what remains is a balance sheet rewrite. The old model absorbed variability with human buffers: teams that could be spun up or down across devices, retail, media, and operations. The new model replaces that elasticity with software agents and rented compute. The fixed costs move from salaries to silicon and energy contracts. For a company with Amazon’s scale, this isn’t just a productivity play; it’s governance. Software is easier to standardize, monitor, and replicate globally than thousands of idiosyncratic processes managed by dispersed teams.

The consequences compound. Once reporting, compliance, ad ops, and content workflows are mediated by agents, every incremental unit of work looks like a throughput question, not a staffing one. The internal labor market shrinks to roles that either build the automation, verify it, or keep the physical plant humming. Everything else becomes an API call. That’s why yesterday’s coverage matters: it is the largest fresh publication to explicitly connect a five‑figure corporate layoff to AI adoption, and it shows how quickly the employment center of gravity can move when the infrastructure spend is already queued.

What to watch next

Expect the quiet parts to get louder. Power procurement will start appearing in investor narratives alongside user growth. Cities will measure economic development in data‑center footprints even as downtown office towers shed tenants. Inside enterprises, the internal “90‑day window” will become a recurring fixture as AI agents expand from drafting and summarization into decision support and autonomous resolution. And yes, more reductions could arrive through 2026—because once a company reframes its operating model around AI‑first processes, the cost of keeping parallel human workflows rises every quarter.

Yesterday’s story crystallized the trade: headcount down across many corporate functions; AI and infrastructure spend up. It’s not a slogan. It’s an org chart etched in silicon, backed by concrete, copper, and gigawatts—and it redraws the map of where work lives.