The Paychecks That AI Built

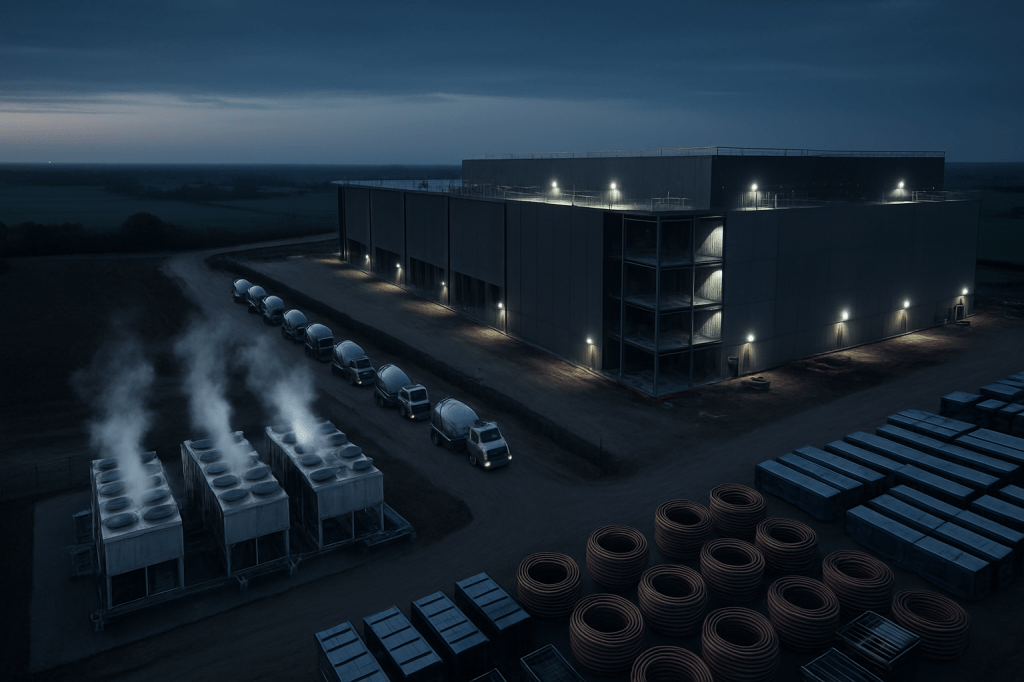

Walk the edge of any county now sprouting server barns and transmission towers and you can hear the sound of artificial intelligence before you ever see a line of code. It’s the hum of temporary chillers, the rattle of ductwork, the steady rhythm of concrete trucks backed up before sunrise. For all the discourse about large language models replacing keystrokes, yesterday’s most important data point came from the other end of the AI stack: the people pulling wire, balancing air, and pouring pads are getting paid more where the data centers rise fastest.

Gusto’s chief economist Andrew Chamberlain cracked open anonymized payroll records from more than 400,000 small and midsize firms between December 2023 and December 2025 and pointed the analysis at the places with the greatest data-center buildout. Define those “hotspots” as the top decile of U.S. counties by total data‑center power capacity, an industrial-strength proxy compiled from facility listings. Then ask a simple question: what’s happening to pay and hiring for the trades that make these facilities real?

The answer is not subtle. Across seven closely tied occupations—electricians; HVAC mechanics and installers; construction managers; plumbers, pipefitters, and steamfitters; welders; cement masons and concrete finishers; and drywall/ceiling installers—workers in these hotspot counties earn a 7.1% wage premium over peers elsewhere. Control for cost of living, occupation mix, and firm size and a 5.8% premium remains, statistically significant and stubborn. In a labor market that’s spent two years nursing its way back to normal, that’s a flare in the sky.

Scarcity, Itemized

The premium isn’t evenly distributed. Plumbers and pipefitters—vital to the cooling systems that keep racks alive—sit at the top with roughly a 20% bump. Construction managers, who orchestrate the choreography of trades and schedules on time-sensitive buildouts, show a 7.3% premium. HVAC mechanics, responsible for a data center’s most power‑hungry organ, land around +4.3%. Welders trail on the level premium but are posting the fastest recent wage growth, a tell that steel and supports are still moving at pace. Electricians look flat to slightly negative in this small‑business dataset (about −2.5%), a quirk that likely reflects unionized work captured by other payroll systems more than a real decline in demand for power pros.

Hiring tells a second story, one about the calendar of construction. Nationwide, skilled‑trade employment has been expanding briskly—on the order of 25–28% year over year. But in hotspot counties, late‑stage roles are exploding: drywall installers are being hired 112% faster than in non‑hotspots, and HVAC mechanics 41% faster. That’s the signature of buildings moving from shell to fit‑out, a wave of finish work and climate control deployment that arrives just before the first workloads flicker to life.

The People Behind the Boom

The composition of this workforce matters. Hotspot hiring skews a little younger—Gen Z accounts for 31.9% of new hires versus 31.2% nationally—and a bit more diverse, with Hispanic workers making up 31% of hires compared to 24% elsewhere among small businesses. Those are narrow deltas, but together they suggest that the AI infrastructure boom is acting as an on‑ramp for the next generation of tradespeople and widening the aperture of who participates. In a tech economy that often conflates “talent” with “degrees,” this is a reminder that mastery with copper, concrete, and compressors is as much a lever of progress as any algorithm.

What the Premium Really Signals

Chamberlain is careful to note the study is correlational. Even so, the pattern is classic microeconomics: when demand outpaces the supply of specialized labor, prices move. AI’s physical plant is now bidding for a scarce set of skills, and the bid-ask spread is visible in paychecks. That ripples up the stack. Higher wages and tighter schedules push project costs higher; project costs shape the delivered price of compute; and compute prices, in turn, influence how aggressively companies ship AI features and where marginal workloads land. The current conversation about GPU scarcity has a quieter twin: the scarcity of the people and trades that make those GPUs useful at scale.

There’s also a geographic story hiding in the method. By tying results to counties with the most installed or planned data‑center power capacity, the analysis is effectively mapping the new industrial heartlands of AI. These are places where grid interconnects matter more than venture density, and where permitting calendars can move more value than product roadmaps. If you want to understand the rhythm of AI deployment over the next two years, drywall and HVAC hiring trends may be as instructive as model benchmarks.

Downstream Consequences

For labor markets, the implications are direct. A durable premium draws workers toward trades schools and apprenticeships, but training pipelines don’t retool overnight. States that streamline licensing reciprocity, expand apprenticeship slots, or modernize career‑technical education will capture more of this upside. Immigration policy—often debated in the context of software talent—suddenly matters for pipefitters and welders, too. And yes, unions will shape the trajectory: the electrician anomaly in this small‑business dataset is a data‑collection artifact, not an economic outlier. Big‑ticket electrical work on hyperscale sites isn’t disappearing; it’s often booked through employers the dataset doesn’t see.

For operators and investors, there’s a bigger strategic note. As AI workloads scale, the bottleneck is not just silicon or power; it’s also sequence. When drywall hiring spikes 112% faster in hotspots, that implies many facilities are crossing the same finish line at once, creating synchronized demand for commissioning teams, interconnect crews, and ultimately operations staff. If the build cycle continues at this cadence, maintenance and retrofits will become a steady, local economic base. If it stutters, counties that scaled up for the boom will need backfills—retro-commissioning, grid upgrades, or different industrial tenants—to avoid a classic bust.

And for climate math, the numbers are double‑edged. The more data centers the world builds, the more obsessively we will need plumbing, heat exchange, and air handling done right. The 20% premium for those who move water and refrigerants is an implicit carbon hedge: better‑paid, harder‑to‑hire specialists who can wring efficiency out of mechanical systems that will otherwise lock in years of waste. Pay attention to where that premium lands; it’s where thermal reality meets digital ambition.

Reading the Tea Leaves

It’s tempting to tuck this into the neat parable that AI takes white‑collar work and gives back blue‑collar jobs. The truth is more layered. What this study really shows is that the AI economy is lumpy, physical, and path‑dependent. Before a single inference runs, there are welds that must not fail, slabs that must not crack, voltages that must not sag, and chilled water that must not stop. Wages are rising where those constraints bite the hardest. That is not a side story to AI. It is the story of how AI becomes real.

If you want a leading indicator of where the next tranche of compute will come online, don’t just watch GPU shipments or cloud earnings. Watch where plumbers are suddenly earning 20% more, where HVAC crews are booked out for months, and where small contractors are hiring drywall installers at twice the national pace. That’s the sound of intelligence being built, one paycheck at a time.